What’s the context?

Climate reporting and disclosure requirements have evolved rapidly in recent years and continue to do so. Understanding and meeting these obligations is essential for pension trustees.

“The science is clear. Nature is deteriorating globally, and biodiversity is declining faster than at any time in human history.”

– The Recommendations

The Task Force on Nature-related Financial Disclosures (TNFD) was launched in June 2021. It developed a voluntary risk management and disclosure framework for organisations to report and act on nature-related risks, with the aim of supporting better risk mitigation and management.

The framework is intended to be used by organisations of all sizes and across all jurisdictions to “identify, assess, manage and, where appropriate, disclose nature-related issues”.

It can be applied by a company in relation to its own activities or by asset owners, including pension schemes, to better understand the nature-related risks affecting the organisations they invest in.

The TNFD final framework was published on 19 September 2023 and contains 14 disclosure recommendations (the Recommendations). The Recommendations help organisations build on their reporting and provide useful information to investors and other providers.

The TNFD mirrors, and sits alongside, the Task Force on Climate-related Financial Disclosures (TCFD) and its own related disclosure and reporting requirements.

For details on the TCFD, see Climate disclosures

The Recommendations aim to be consistent with other initiatives and frameworks. In particular, they align with the International Financial Reporting Standards (IFRS) developed by the International Sustainability Standards Board (ISSB). Other aligned initiatives include the Global Reporting Initiative’s (GRI) Sustainability Reporting Standards, the European Financial Reporting Advisory Group and the UN Kunming-Montreal Global Biodiversity Framework (GBF).

The Recommendations and additional guidance provide a basis for organisations to identify, assess and disclose their nature-related dependencies, impacts, risks and opportunities consistent with the ISSB and GRI standards. They are intended to provide a practical way for organisations to get started and to increase the scope and ambition of their disclosures in coming years.

Understanding nature-related issues

“It is essential to evaluate dependencies and impacts on nature to assess the risks and opportunities to an organisation.”

– The Recommendations

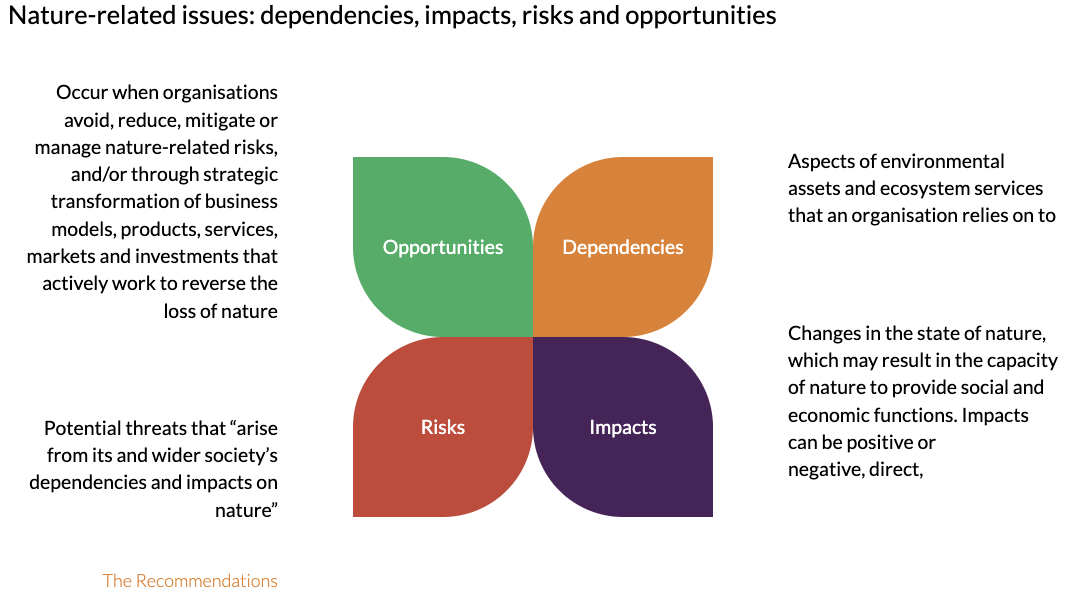

The Recommendations are intended to help organisations meet the challenge of assessing and managing the impact of nature on society, the economy and financial systems, and to report on nature-related:

- dependencies

- impacts

- risks, and

- opportunities

These four concepts are collectively referred to as nature-related issues.

What are my compliance obligations?

Pension schemes are not yet required to make nature-related disclosures in line with the Recommendations. Consequently, it is arguably still too early for schemes to put in place any detailed approach to identify and address nature-related issues.

However, given the direction of travel on ESG, disclosures in line with the Recommendations may become a statutory requirement in the future. The Government announced in its Green Finance Strategy that it would explore the best way to incorporate the Recommendations in the UK.

Some organisations have already signed up publicly to the Recommendations. The TNFD maintains a list of organisations that have committed to start making disclosures aligned with the Recommendations.

Trustees wanting to get ahead of the curve may wish to engage with investment managers and advisers to understand:

- how nature-related issues are being considered in their decision-making, and

- whether they may be financially material.

From TCFD to TNFD: potential challenges

The TNFD Recommendations are based on the same four pillars used in the TCFD framework: governance, strategy, risk, and metrics and targets. The TNFD has carried over all the TCFD recommended disclosures, as well as adding three new ones.

The TNFD framework will be a familiar structure for trustees already reporting under the Occupational Pension Schemes (Climate Change Governance and Reporting) Regulations 2021 (the Climate Reporting Regulations).

Trustees might, therefore, think that it ought not to be too much of a stretch to bolt on TNFD to their TCFD governance processes and reporting.

However, although the frameworks are indeed very similar, the detail of TNFD, when compared with TCFD, is likely to pose some significant early challenges for all but the most committed, and well resourced, pension trustee boards.

What to measure and how – metrics

This is the most obvious challenge for trustees looking at the Recommendations. The Climate Reporting Regulations specified a limited number of climate-related metrics which trustees were expected to measure and disclose against. These included carbon footprint and a portfolio alignment metric.

Although data availability and quality have posed some challenges, and there are variations in methodology, the Department for Work & Pensions was clear on what trustees were expected to monitor and report.

Nature-related metrics are more nascent and multi-faceted. It will be much harder for pension trustees as asset owners to get to grips with. As nature-related issues are so complex, there are many more things that can be measured and at a potentially very granular level.

Across certain industry sectors, such specific metrics may be useful indicators of risk and opportunity relating to particular investee companies. For example, concentrations of key pollutants in wastewater may be a pertinent metric for certain industries. But it may not be so meaningful for pension schemes. For most, this level of analysis will be too detailed.

We anticipate that trustees will need to be more discerning in their approach to such metrics. We expect that those who are first embarking on a TNFD journey will have to start by building confidence in the ability of their appointed managers to obtain, interpret and act on such detailed metrics – and more particularly those managers’ specialist research teams – rather than the trustees carrying out this role themselves.

To a certain extent, the TNFD has anticipated that the lot of an asset owner will not be an easy one when it comes to nature. As such, the Recommendations are supplemented with specific industry guidance for various industry sectors, together with discussion papers aimed at financial institutions. These focus on the landscape of biodiversity and approaches to advanced scenario analysis.

The guidance and discussion papers set out specific guidance for banks, insurers, asset managers and asset owners, recommending some higher-level metrics for those organisations to measure and report against. These include the portfolio’s exposure to sectors or companies with material dependencies on nature.

These may make more sense for a pension scheme, but there is still some way to go before such metrics coalesce into anything as uniform as some of the more established metrics for climate.

Targeting nature-positive impacts

Another way TNFD differs from TCFD for pension trustees is in its greater focus on nature-related “impacts” as well as risks. Those looking to adopt the Recommendations should be seeking to identify, assess and manage not only the risks that nature-related issues might pose to them but also the external impacts that they might have on nature. This raises a fundamental point for trustees.

It is well understood that trustees can act on any matters that go to financial risk and returns for their investment portfolios, and that these can include environmental risks, both climate and nature-related. To that extent, the Recommendations on monitoring and managing nature-related risks will chime with how trustees have approached climate-related risks under the TCFD.

Where there is portfolio exposure to sectors with material dependencies on nature, and these in turn create a financial risk to the portfolio, trustees will want to understand such risks in the same way as they should consider those parts of their asset portfolio with high exposure to climate transition risks.

However, care is needed when looking at the external impacts that investee companies have on society and their environments. Where there is no direct financial impact on a scheme’s portfolio, trustees might find they face challenges over whether this falls within their fiduciary duties, particularly if they wish to start setting impact targets.

In practice, asset owners subject to fiduciary duties will usually seek to square the circle by acting on an investment belief that companies that “do good” ought also to “do well” as a financial proposition. But this needs to be evidence-based, and it will be particularly important that trustees take care and advice to ensure that they are acting consistently with their legal duties when approaching this particular aspect of the Recommendations.

None of this should be a reason not to engage with the issues, but a realistic approach as to what is achievable is likely to be required from any early-mover trustee boards.

What are the latest developments?

In September 2025, the TNFD released its first status report. The report highlights many statistics relating to the implementation of TNFD, including:

- 620 organisations from over 50 countries or areas have publicly committed to getting started with nature-related reporting aligned to the TNFD recommendations

- evidence of over 500 first- and second-generation TNFD reports are now published

- over 60% of companies and financial institutions surveyed for the report believe their nature-related issues are as significant, or more significant, than climate-related issues to the future prospects of their business, and

- 78% of those companies that have already reported have integrated the presentation of their climate and nature reporting.

In November 2025, the IFRS Foundation’s ISSB announced that it would begin work on standard setting for disclosure requirements on nature-related risks and opportunities, with plans to have an initial draft released by late 2026.

The ISSB said the new initiative was being undertaken in response to identified investor needs for nature-related disclosures. It has not yet decided if it will develop a new standalone standard, amend its current standards with new reporting requirements, or take another potential approach.

The TNFD said it would complete all its technical work in progress, including the development of additional sector guidance, by Q3 2026, and refrain from developing further guidance as it switches to focusing on supporting the ISSB’s work programme.

Also in November 2025, the TNFD published guidance on incorporating nature into corporate transition plans, providing a structured framework for managing nature-related risks and opportunities alongside climate objectives.

Nature transition plans are defined as organisational strategies to halt and reverse biodiversity loss by 2030, aligning with the GBF.

Organisations can use transition planning to reduce negative nature impacts, protect and restore ecosystems, and address underlying drivers of nature loss while managing synergies and trade-offs with climate goals.

For more on what transition planning means for pension schemes see Transition plans